248.335.7211

248.335.7211For long-term investment goals such as retirement, time can be one of your biggest advantages. That's because time allows your investment dollars to do some of the hard work for you through a mathematical principle known as compounding.

The snowball effect

The premise behind compounding is fairly simple. You invest to earn money, and if those returns are then reinvested, that money can also earn returns.

For example, say you invest $1,000 and earn an annual return of 7% — which, of course, cannot be guaranteed. In year one, you'd earn $70 and your account would be worth $1,070. In year two, that $1,070 would earn $74.90, which would bring the total value of your account to $1,144.90. In year three, your account would earn $80.14, bringing the total to $1,225.04 — and so on. Over time, if your account continues to grow in this manner, the process can begin to snowball and potentially add up.

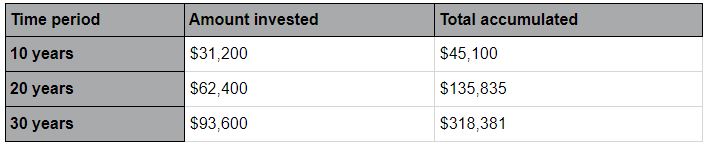

Time and money

Now consider how compounding works over long time periods using dollar-cost averaging (investing equal amounts at regular intervals), a strategy many people use to save for retirement.1Let's say you contribute $120 every two weeks. Assuming you earn a 7% rate of return each year, your results would look like this:

After 10 years, your investment would have earned almost $14,000; after 20 years, your money would have more than doubled; and after 30 years, your account would be worth more than three times what you invested.2 That's the power of compounding at work. The longer you invest and allow the money to grow, the more powerful compounding can become.

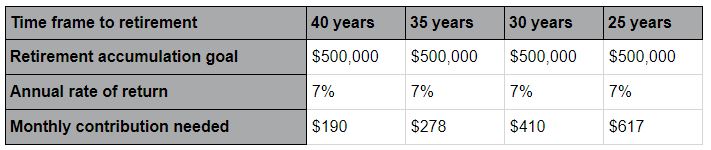

The cost of waiting

Now consider how much it might cost you to delay your investing plan. Let's say you set a goal of accumulating $500,000 before you retire. The following scenarios examine how much you would have to invest on a monthly basis, assuming you start with no money and earn a 7% annual rate of return (compounded monthly).

So the less time you have to pursue your goal, the more you will likely have to invest out of pocket. The moral of the story? Don't put off saving for the future. Give your investment dollars as much time as possible to do the hard work for you.